Reminder to self: tax code on NSOs, ISOs, and RSUs

Here are three common types of equity grants:

- NSOs (Non-qualified Stock Options)

- ISOs (Incentive Stock Options)

- RSUs (Restricted Stock Units)

Your employer may give you one of these as part of your compensation package. They work differently, and more importantly, they are taxed differently. I'm writing this mostly as a reminder to myself, so below is the simple version of how each one gets taxed. Ultimately, it boils down to one idea:

The IRS taxes equity compensation when value becomes yours, and then taxes any later investment gain or loss when you sell.

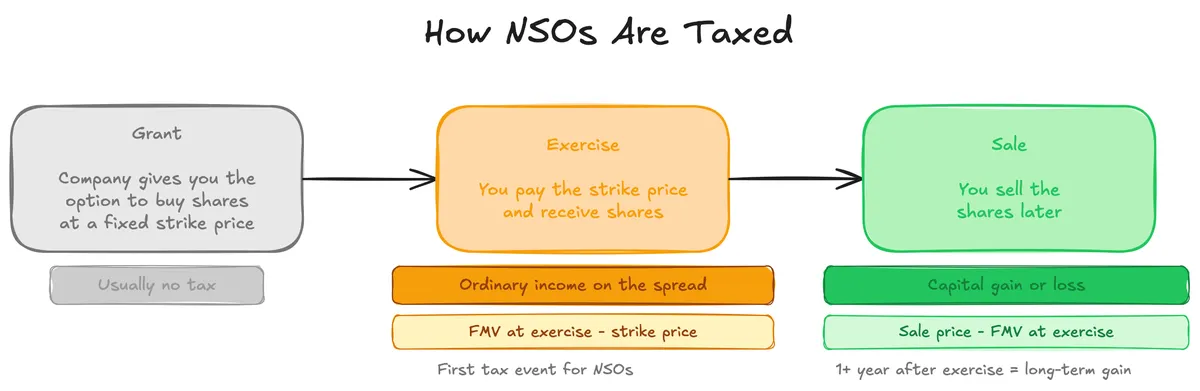

NSOs

- Grant: Usually no tax.

- Exercise: The spread between fair market value and strike price is ordinary income.

- Sale: Any price change after exercise is capital gain or loss. More than 1 year after exercise is generally long-term.

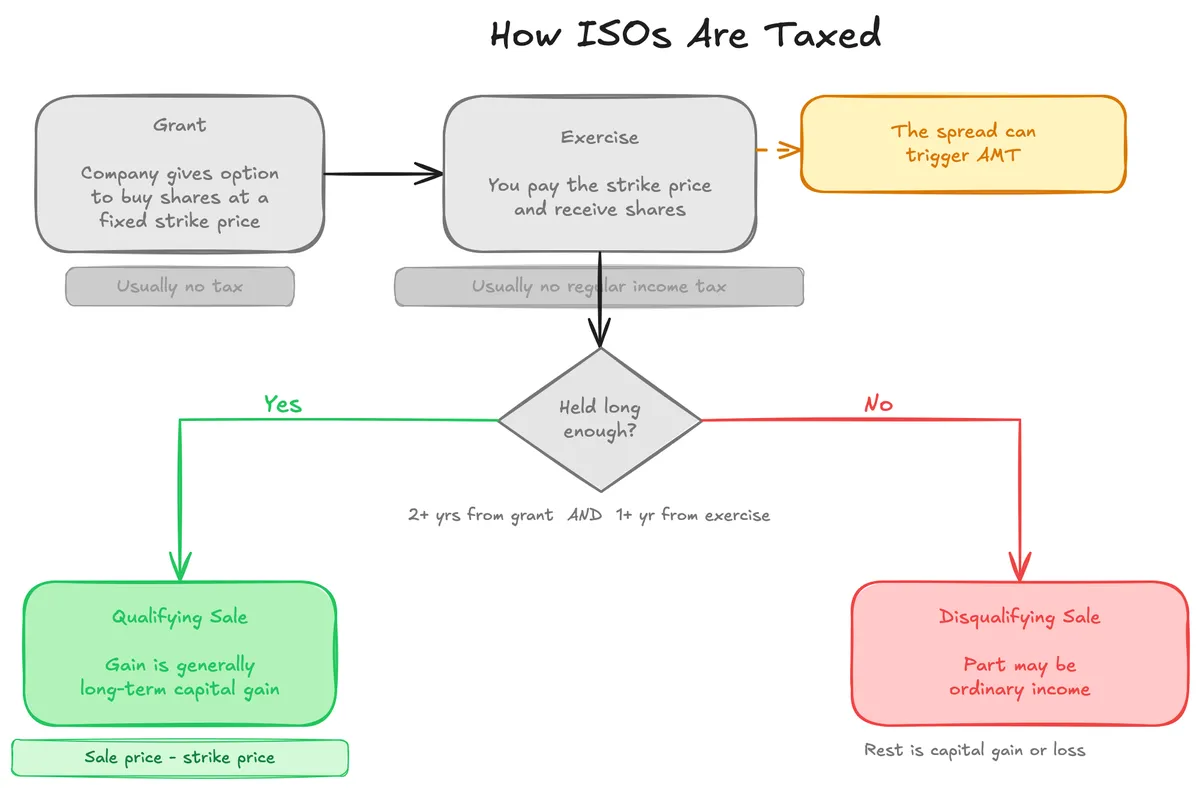

ISOs

- Grant: Usually no tax.

- Exercise: Usually no regular income tax, but the spread can trigger AMT.

- Sale: If you sell at least 2 years after grant and 1 year after exercise, the gain is generally long-term capital gain. If you sell earlier, part of the gain may be ordinary income.

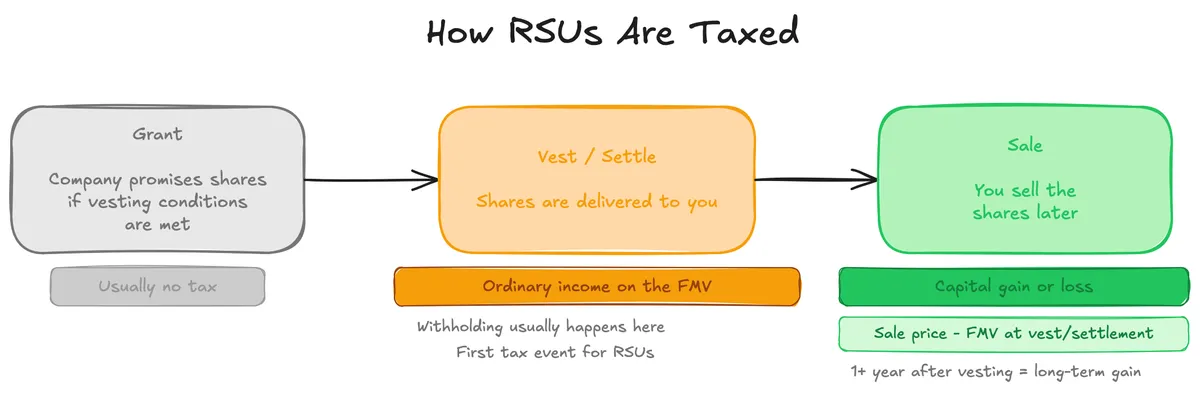

RSUs

- Grant: Usually no tax.

- Vesting/settlement: The fair market value is ordinary income and is usually subject to withholding.

- Sale: Any price change after vesting/settlement is capital gain or loss. More than 1 year after vesting/settlement is generally long-term.

Why Companies Use Each

- NSOs: Used when the company wants more flexibility, or when the recipient is not eligible for an ISO. Common examples include consultants, advisors, directors, and grant amounts above ISO limits.

- ISOs: Usually for employees when the company wants to offer potential tax advantages. But ISOs come with stricter rules, so not every grant can qualify.

- RSUs: More common at larger, later-stage, or public companies. They are simpler to understand than options and do not require the employee to pay an exercise price.